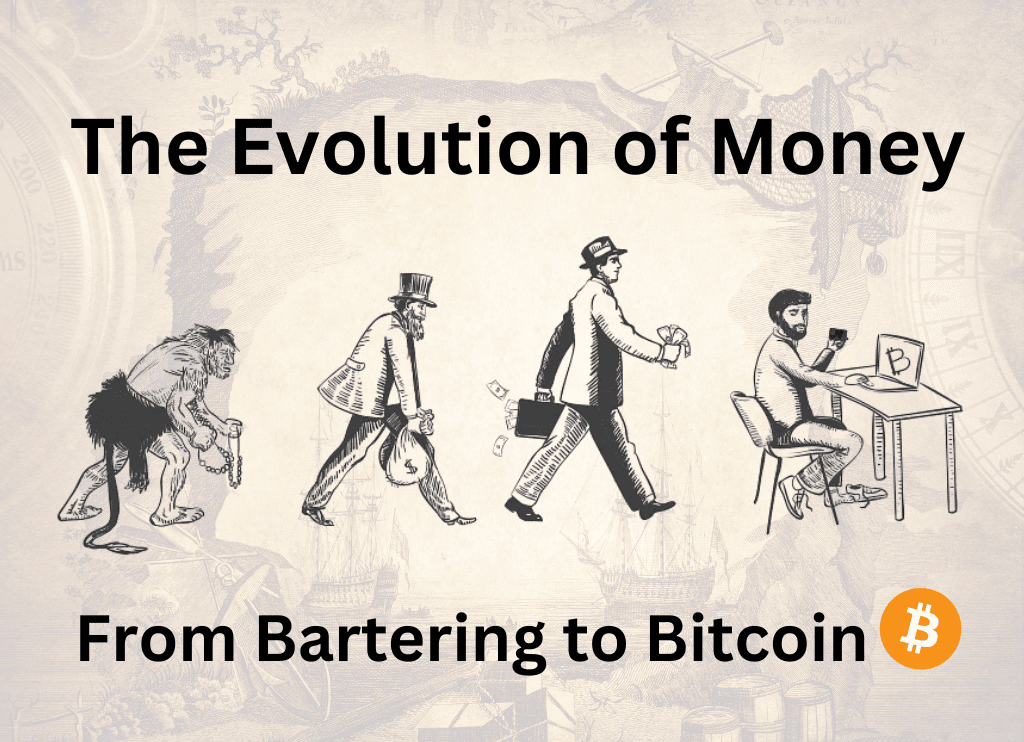

Since it serves as a means of exchanging goods and services, money is a crucial component of human society. Throughout human history, the idea of money has undergone a major metamorphosis as it has adapted to fit the shifting demands of civilizations. In this article, we’ll look at the history of money, from the first examples of trading until the invention of Bitcoin, the first decentralized digital currency.

Bartering: Where Did Money Come From?

The first exchanges of commodities and services took place when humans bartered with one another in prehistoric times. Bartering is the direct trade of products or services without the use of a middleman like money. For instance, a blacksmith may exchange a sword for a quantity of grain or a farmer might exchange a basket of apples for a deer hide.

Although bartering was a successful method of exchange for goods and services, there were some restrictions. It wasn’t easy to locate someone who wanted what you had to offer and had something you wanted in exchange, for one thing, because not all products were of equal value. Additionally, trading needed a double coincidence of wants, which implied that both parties had to desire what the other had to offer concurrently. Bartering became time-consuming and ineffective as a result.

Metal Coins: The Original Form of Money

Early civilizations started using metal coins as a medium of commerce to get beyond the limits of bartering. Around 700 BCE, the first metal coins were produced in Lydia (present-day Turkey), and they were made of electrum, a naturally occurring alloy of gold and silver. As the usage of metal coins grew over time, various civilizations started to mint their own coins with distinctive patterns, symbols, and inscriptions to set them apart from those of other civilizations.

Compared to bartering, using metal coins had a number of benefits. Coins made trading goods and services easier because they were portable and simple to transfer. Coins were a perfect store of value since they were made of valuable metals and had intrinsic value. Finally, the weight and purity of coins were regulated, making them more dependable and practical to use than bartering.

Paper Money: Fractional Reserve Banking’s Ascent

Paper money first appeared as societies expanded and the need for money grew. Known as “flying money,” paper money was originally utilized in China during the Tang period (618–907 CE). Because it was lighter and simpler to carry than metal coins, paper money was more practical than coins made of metal, but a valuable good like gold or silver did not back it. Paper money was instead backed by the issuing authority’s pledge to swap it for a set number of metal coins.

Fractional reserve banking, in which banks would issue more paper money than they held in metal coins in reserve, was made possible by the usage of paper money. Banks were able to boost the money supply thanks to fractional reserve banking, which in turn promoted trade and economic expansion.

However, there were drawbacks to using paper money as well. For starters, inflation resulted from the expansion of the money supply as the value of the currency in circulation decreased over time. Paper money was also easy to counterfeit, which reduced public confidence in the currency. Many nations later switched to a gold standard, where the paper money was backed by a set quantity of gold kept in reserve, to allay these worries.

Electronic money: a modern concept

The introduction of computers and the internet has brought about yet another change in how we use money. The term “electronic money,” usually referred to as “digital money,” describes currency that is available in digital form and may be sent electronically. Due to the absence of tangible checks or currency, this form of money has improved efficiency and convenience in financial transactions.

The credit card, which eliminated the need for carrying currency when making purchases, was among the first types of electronic money. With the advent of electronic funds transfer (EFT) systems, money could be moved between bank accounts without requiring a trip to the bank or the use of a cheque.

New electronic payment methods like PayPal, which allowed users to send and receive money via the internet, were introduced with the development of the internet. E-commerce expanded as a result of the ease with which consumers could now purchase and sell products and services online thanks to PayPal and other online payment systems.

Electronic money was convenient, but it still relied on centralized organizations to oversee and safeguard transactions, including banks and payment processors. The risk of fraud and the potential for government involvement were just two of the difficulties brought on by this centralization.

Bitcoin: The Start of Decentralized Digital Currency

The first decentralized digital currency, known as Bitcoin, was launched in 2009 by an unidentified person or group of individuals operating under the pseudonym Satoshi Nakamoto. Peer-to-peer technology, such as Bitcoin, enables safe, direct-value transactions between people without the use of middlemen.

Utilizing blockchain technology, a decentralized ledger that keeps track of all Bitcoin transactions is one of Bitcoin’s fundamental inventions. This ledger is kept up to date by a network of computers and makes sure that transactions are safe and unchangeable. With a limited number of 21 million coins, Bitcoin is also intended to be deflationary, which aids in preserving its value over time.

People now have more power over their own finances thanks to the disruption caused by bitcoin and other cryptocurrencies to the established financial system. Traditional financial systems cannot match the level of anonymity and security provided by cryptocurrencies, which are also free from government meddling or regulation.

Conclusion

The shifting demands of human society have influenced how money has evolved. Money has evolved to fulfill the demands of its users, from the earliest forms of trading through the arrival of decentralized digital currencies like Bitcoin. Although the direction of money is unclear, it is evident that the trend toward decentralization and increased financial independence will continue to influence the financial environment.